Dynamic Rate, Mvmt. I

Q170. A recent governance proposal (offers a dynamic Earn Rate as one solution to the problem of Anchor Protocol’s sustainability.

Assigning the above, if we define a 1 month period in which to measure the change of yield reserve delta and a 3% rate for the delta threshold, we can get the following formula that runs every month:

(% Earn Rate Change) = ( (Yield Reserve % Change) - 3%)

Further, to ensure maximum stability in the earn rate, we could limit the amount the earn rate can increase or decrease per period to 1.5%. From this we can get the following formula:

(% Earn Rate Change) = min( abs(1.5%, ((YR % Change) - 3%)) )

So for example, if the yield reserve increased by 5% in the period of one month:

X = min( abs(1.5%, (5% - 3%))) = min(1.5%, 2%) = 1.5%

The earn rate would increase by 1.5%, conversely, if it dropped by 5% the earn rate would drop by 1.5%.

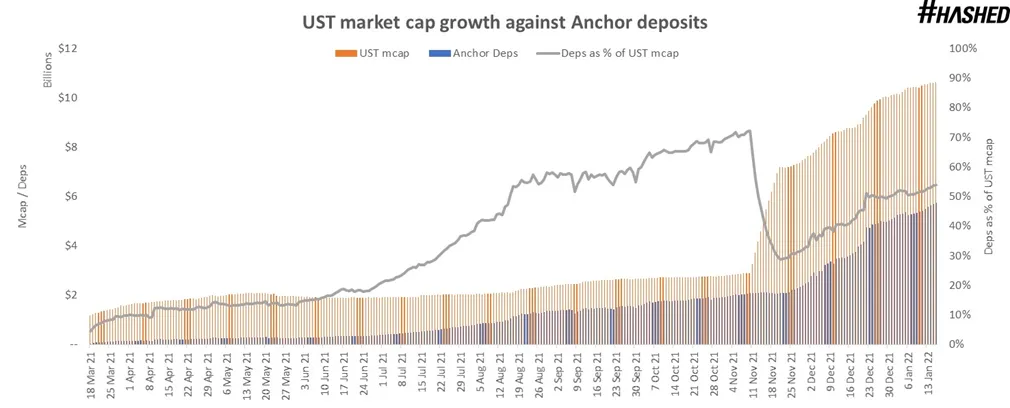

Deposits As Anchor grows in TVL, it is not expected that they grow at the same rate as before. To illustrate my point, if current deposits total were to grow by 10% weekly for the next 52 weeks, Anchor would have $818b in deposits, more than the current market cap of Bitcoin ($740b at the time of writing). As such, the approach to forecasting deposits growth rate will not be based on historical growth rates. It will be a function of Anchor’s deposits as a % of total UST market cap.

At Anchor’s launch, Anchor had $53m in deposits and UST’s market cap was $1.2b — giving a ratio of 4.5%. Currently, Anchor has $5.8b in deposits against UST’s market cap of $10.7b — ratio of 54%. The grey line in the chart plots Anchor deposits as a % of UST’s market cap over the course of Anchor’s lifecycle. It is more realistic that as UST scales towards mass adoption, the proportion that flows into Anchor follows accordingly. Since 18 March 21, UST grew at a CWGR of 5.2% and Anchor’s deposits were on average 37% of UST’s market cap. However, this was weighed down by lower percentages in earlier months due to lack of awareness. The average ratio was 52.5% in the last 6 months (Aug 21 onwards) and we believe the forecasted figure will resemble that range. In the base model, UST is expected to grow at 3.5% weekly and Anchor consumes 55% of UST market cap at any point in time.

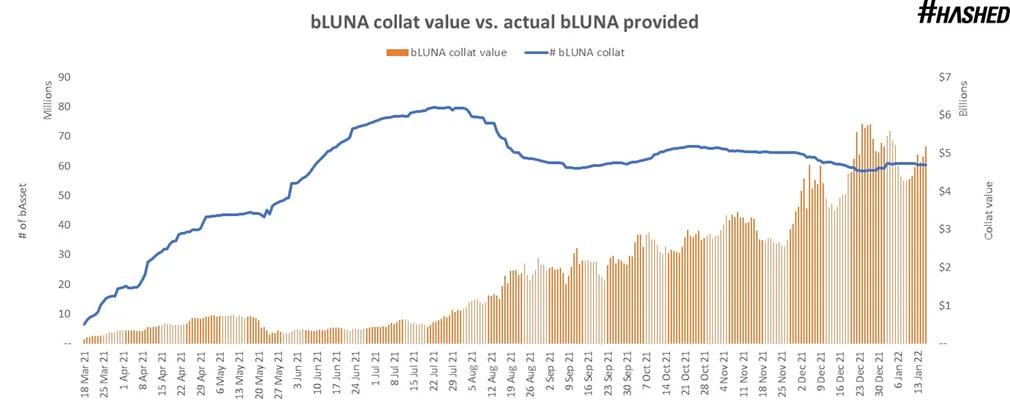

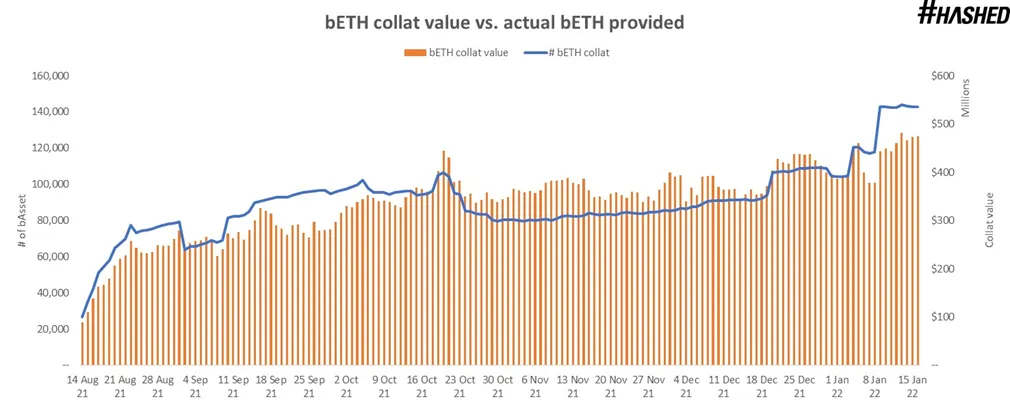

Collateral Collateral value had a historical CWGR of 9.3%, but a large part of that growth could have been due to the surge in LUNA’s and ETH’s prices. The more accurate approach to projecting collateral growth rates is to strip out the impact of the collateral’s price. The charts below (blue line) shows how much actual bLUNA and bETH were provided to Anchor as collateral.

bLUNA grew by 5.3% weekly while bETH grew by 4.4% weekly (based on CWGR). However, the growth of bLUNA has remained stagnant in recent months while bETH has shown gradual increases. With the rise of Terra dapps giving more use cases and differing yields for LUNA, it is expected that fewer users would want to sacrifice their LUNA as collateral for Anchor over time. Seeing the actual growth rates of number of bLUNA and bETH used as collateral gives us a clearer picture of forecast growth rates.

Model output

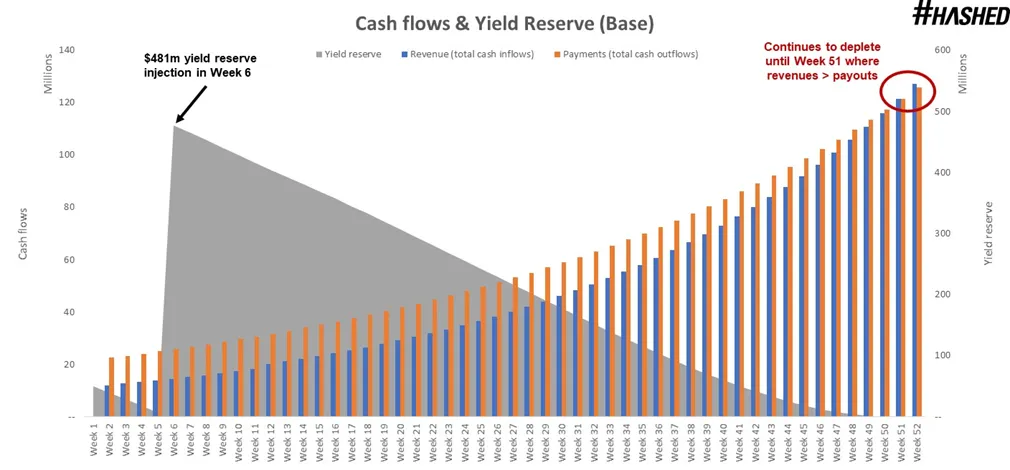

Base

In the base case, the yield reserve is only sustainable until Week 6 (that is, ~20 Feb at the time of writing). Thereafter, a top-up of c.$481m is required to keep Anchor functioning. At the base case projected rates for deposits, collateral and borrows, Anchor continues to deplete the yield reserve until Week 51 where cash inflows finally grow more than outflows. Self-sustainability may then be achieved, assuming the terminal growth rates hold.

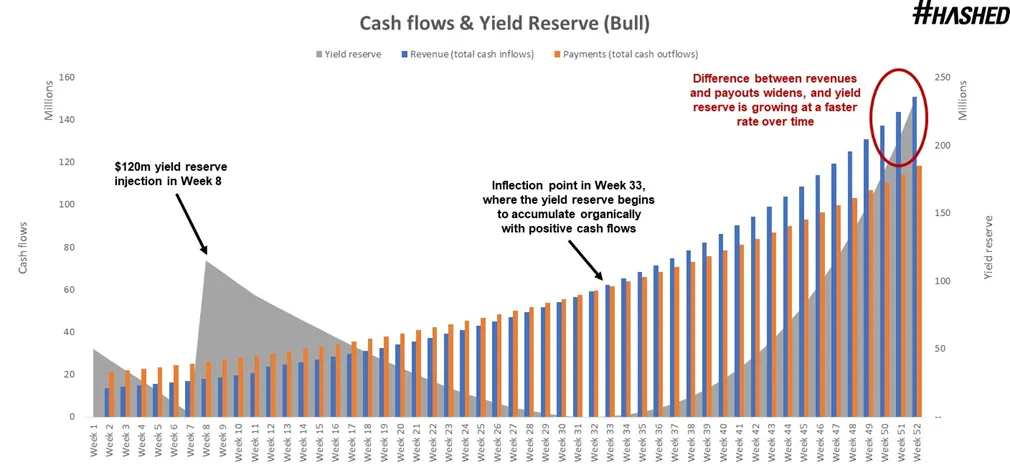

Bull

The bull case requires a c.$120m yield reserve top-up at a slightly later date in Week 8, since the gap between revenues and payouts are smaller in earlier weeks. It continues to deplete until Week 33, as that is when revenues turn positive over payouts and Anchor hits an inflection point. In later weeks, the optimistic scenario indicates cash inflows outpacing outflows so Anchor is able to provide yield on a self-sustainable basis.

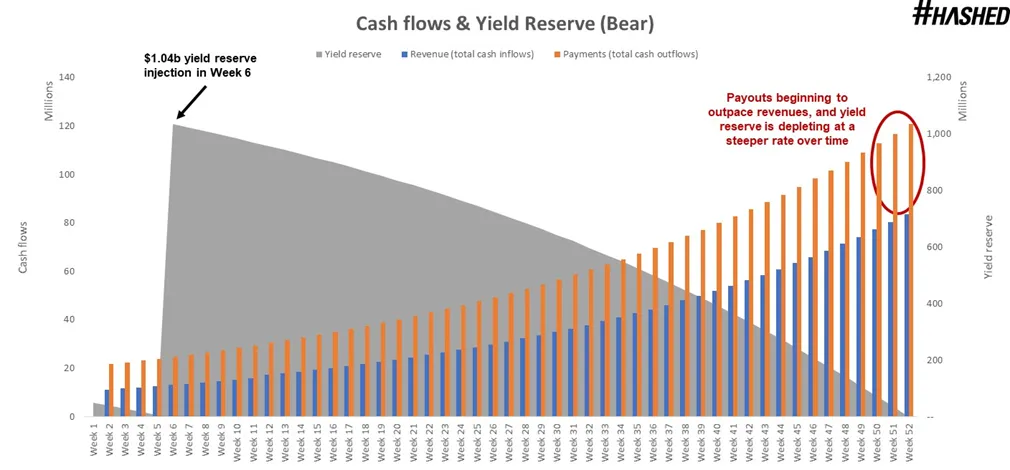

Bear

In the bear case, a large yield reserve top-up of c.$1.04b is required to keep Anchor sustainable for the 52-week forecast period. In fact, there is no indication that Anchor eventually achieves self-sustainability since the steepness at which the yield reserve is depleting increases over time. Since payouts continue to outpace revenues, Anchor has a growing cash burn rate and continues to market negative net cashflows. This may result in another top-up required at the end of the forecast period.

Conclusion

There is about 30–35 days left before the yield reserve is fully depleted (as at the time of writing). The model projects cashflows on a weekly basis while in reality, cashflows are transacted on a block-by-block basis. Based on the model’s base case, a yield reserve top-up of $481m is required before Anchor is able to achieve self-sustainability after 51 weeks (assuming growth rates hold). Anchor is only 10 months old and has managed to record >$10b in TVL. This ranks them as the second largest lending protocol on the blockchain, behind Aave which has been around for >4 years (previously known as ETHLend).