$MATIC Liquid Staking

Define what liquid staking is in your words, and evaluate the different liquidity staking options based on three different metrics of your choice. Bonus: How do people use these "liquid" derivatives? Do you see any trends?

Key Highlights

- The total amount of Matic staked is 3.3 Billion of the 10 Billion in supply. However, the top liquidity staking services account only for 2.7%. Majority of which is held by Lido.

- Lido has the highest staked amount, accounting for 1.5% of the staked Matic.

- The price of Lido token ( stMATIC) is the mostly closely pegged to Matic while claystack’s (csMATIC) differs from the price of matic.

- Lido finance and stader delegate to 6 and 5 validators respectively thereby reducing the chances of slashing. However, claystack and ankr delegate to only 1 validator each and rather focus on APY. This increases the risk associated with staking.

- Service providers cannot be judged only by their APY and transaction count, but the use case for their staked token is equally important. stMatic from Lido appears to be the most integrated. With it being used across a number of defi and DEX apps.

Objective

The article dives deep into liquidity staking on Matic and assess the different service providers present in the market.

They are mainly evaluated on the basis of

- Market share

- Popularity among users

- Trend analysis

- Price analysis of liquid staking token

- Validator exposure

- Defi integeration

The four horsemen

| Service Provider | Derivative | APY (%) |

|---|---|---|

| Lido | stMatic | 8.676 |

| ClayStack | csMatic | 9.53 |

| Ankr | aMaticC and aMaticB | 9.55 |

| Stader | MaticX | 8.5 |

Analysis

Market Share

Of the 10 Billion Matic token currently in supply, 3.37 Billion token are locked up for staking. However, ==only 2.7 % of these are through liquidity staking==. Additionally, Lido finance and Stader labs make up the other 2.6%, leaving a partly 0.1% to claystack and ankr.

Popularity among users

Observation

When we compare the service providers, we find that ==Lido has the highest number of users== and has also processed the most number of stake requests.

However, Stader labs has the highest median staked amount. Much higher than Lido also.

Additionally, claystack that has the second highest stakes performs poorly when we see the median amount indicating that the small fishes prefer this.

( We use median, to reduce the influence of outliers)

Trend analysis

Observation

We see that there have been bouts of increased staking activity throughout the last 3 months. The August month of 2022 witnessed higher stakes than usual.

The outlier in stake amount related to stader labs, is because of a whale deposit. Transaction : 0xbe48d3f0f9c2ec59c64e41cd2a90ad583a83f37177d64b87bab238a4a008b921

Correlation analysis.

T==he stacking amount and the matic price are weekly correlated in the past 3 months.==

Price analysis of underlying token

Whilst stMatic (or equivalent token) is strictly speaking, not required to trade on par with Matic, many players have built up leveraged stMatic-Matic positions on Aave (and other de-fi protocols) which puts them at risk of liquidation if the price ratio deviates too much from the 1:1 “peg” .

Observation

Hence on evaluating the tokens, we find that Lido token ==stMatic remains most closest to Matic== while aMaticb from ankr performs the most.

Note: we have not included the price of csMATIC because it is missing on the flipside tables, coingecko and coinmetrics as well.

Validator exposure

One of the innate risk associated with liquid staking is that the validator with whom Matic is staked might make a mistake leading to slashing. This results in a loss of funds. Service providers can employ different strategies. One among them is staking MATIC with more than one validator thus reducing risk. However, another strategy would be to stake with validator that provide the highest return.

In case of a system or security failure, validators can suffer penalties where they lose some of their staked funds in a process known as slashing. Making sure you are staking with reputable operators is one way to hedge this risk, another is with slashing insurance.

Observation

Among the service providers, ==Lido delegates the staked amount equally between 6 different validators thus reducing risk,== but this also reduces the return APY. Stader too employs the same strategy.

However, Ankr and Claystack focus more on a higher APY strategy and hence go with the riskier validators. Ankr is among the few service providers who run their own validator system on MATIC.

Defi Integeration

Most important besides stake pool strategy & fees (and arguably most important) is how well integrated a stake pool token is within DeFi. The advantages of liquidity staking is the ability to sell instantly and also provide liquidity in DEX to earn extra income. ( Leveraged farming).

For this to happen, the stake pool token needs to be integrated with different protocols.

Observation

Among all the tokens, ==Lido’s stMatic is the most integerated with more than 10 dapps supporting it.== Stader’s MaticX comes second with 9 dapps support.

ankr’s amaticc and claystack’s csMatic are both supported in 4 dapps each.

Among the dapps, it appears that DEX dapps process much higher volumes than other De-Fi dapps.

Conclusion

- The total amount of Matic staked is 3.3 Billion of the 10 Billion in supply. However, the top liquidity staking services account only for 2.7%. Majority of which is held by Lido.

- Lido has the highest staked amount, accounting for 1.5% of the staked Matic.

- The price of Lido token ( stMATIC) is the mostly closely pegged to Matic while claystack’s (csMATIC) differs from the price of matic.

- Lido finance and stader delegate to 6 and 5 validators respectively thereby reducing the chances of slashing. However, claystack and ankr delegate to only 1 validator each and rather focus on APY. This increases the risk associated with staking.

- Service providers cannot be judged only by their APY and transaction count, but the use case for their staked token is equally important. stMatic from Lido appears to be the most integrated. With it being used across a number of defi and DEX apps.

Shoutouts

- Mehdi#9668 for providing, the validator names. →

- @Rohnin for being the friendly neighborhood

spidermanmod and helping with all doubts on the discord channel - DJ pinanawo for playing awesome music

Important Parameters at a glance

NOTE: The below metrics are service provider specific. Use the above dropdown to change values.

Introduction

Staking is the act of locking up your cryptocurrency in service of a project for a period of time and getting a reward in return. It’s a relatively safe way to earn passive income. But the ever-churning innovation mill that is decentralized finance (DeFI) has come up with a way to have your cake and eat it too -- liquid staking.

With liquid staking, your tokens retain their liquidity despite being staked. It accomplishes this by tokenizing your stake -- you get a staked-ETH token (stETH) for each ETH staked. If you want out, just trade your stETH back for the original token. In DeFi, liquidity is king and this approach has a number of benefits:

-

Users can unstake instantly for a nominal fee, which is not possible when staking directly with validators. This makes proof-of-stake assets more liquid, giving users more financial flexibility.

-

This makes staking more attractive, which contributes to decentralization and security of the blockchain in question.

-

The staking derivatives allow greater composability and can be used as collateral in other DeFi applications to earn additional yield.

Risks associated - -

There is always a chance of a smart contract flaw or vulnerability that can lead to loss of funds and the best protocols offer bug bounties to reduce the risk of a breach.

-

In case of a system or security failure, validators can suffer penalties where they lose some of their staked funds in a process known as slashing. Making sure you are staking with reputable operators is one way to hedge this risk, another is with slashing insurance.

How did i do it ? AKA Methodology

-

To identify the stakes and the unstake activity, we look at the PoS contract

0x5e3ef299fddf15eaa0432e6e66473ace8c13d908. Using the table ethereum.core.fact_token_transfers, we can identify stakes and unstakes based on the direction of matic flow. -

The contract address of different staking service providers-

| Provider | Eth address | Polygon address |

|---|---|---|

| Lido | 0x9ee91f9f426fa633d227f7a9b000e28b9dfd8599 | 0x3A58a54C066FdC0f2D55FC9C89F0415C92eBf3C4 |

| stader | 0xf03A7Eb46d01d9EcAA104558C732Cf82f6B6B645 | 0xfa68FB4628DFF1028CFEc22b4162FCcd0d45efb6 |

| claystack | 0x91730940dce63a7c0501cedfc31d9c28bcf5f905 | 0x7ed6390f38d554B8518eF30B925b46972E768AF8 |

| Ankr | 0x9846c1f06d2f0e7c4678aeea56eb826efe41bb9a | 0x03A97594aA5ecE130E2E956fc0cEd2fea8ED8989 |

-

-

Throughout the article We use median rather than average while caluclating distribution, to reduce the influence of outliers

-

Calculating price change - To calculate the mean deppeg value, we use the fact_hourly_token_prices to extract the price of the stake token. Using

token_price/matic.matic_price we get an estimate. To calulate the average error between matic and stake token, we use avg(abs(difference_daily))*100 as avg_error

-

The stake token is rarely used in the ethereum chain and is thus bridged to polygon network on minting. Hence all the dApps supporting it are present on the polygon chain. Thus, we use the polygon.core.fact_token_transfers and polygon.core.dim_labels dl tables to identify the dApps the tokens interact with.

Glossary

- Service provider : Organizations that aggregate funds from individual investors to invest ( or stake ) in different validators. They usually take a commission out of the rewards. No limits to entry. Example - Lido

- Validators : Entities that operate a chain node that verifies the transactions and mints blocks. Example - StakePool

- stake token - Everytime an user deposits funds into a service providers address, he/she will receive an equivalent value in stake token which can later be used for

-

Yield farming

-

Leveraged trading

-

claiming rewards

\

-

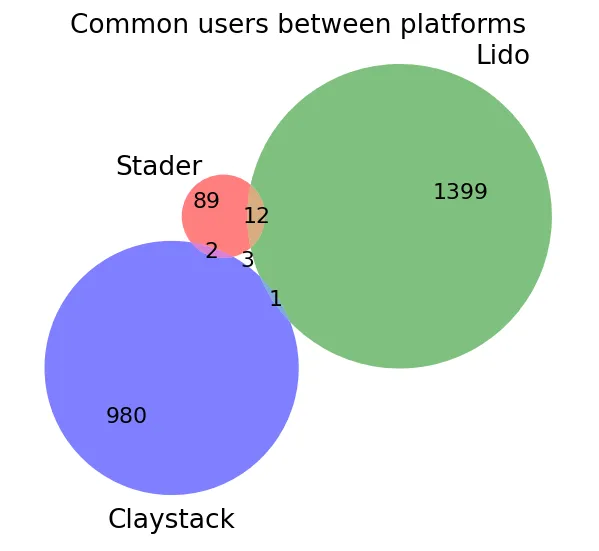

Common users between service providers (platforms)

We observe that the market is quite fragmented and users of one service providers are not users of mulitple projects.

Among those that are, Lido and Stader share 12 customers.

Query-