AAVE Unique Addresses

What is AAVE?

One of a number of emerging DeFi cryptocurrencies, Aave is a decentralized lending system that allows users to lend, borrow and earn interest on crypto assets, all without middlemen.

Running on the Ethereum blockchain (and other blockchains now), Aave is a system of smart contracts that enables these assets to be managed by a distributed network of computers running its software.

Different parts of AAVE

Aave is perhaps best described as a system of lending pools.

Depositors and Borrowers

Users deposit funds they wish to lend, which are then collected into a pool. Borrowers may then draw from those pools when they take out a loan. These tokens can be traded or transferred as a lender wishes.

Like other decentralized lending systems on Ethereum, Aave borrowers must post collateral before they can borrow. Further, they can only borrow up to the value of the collateral they post.

Borrowers receive funds in the form of a special token known as an aToken, which is pegged to the value of another asset. This token is then encoded so lenders receive interest on deposits

Flash Loans

Aave allows certain loans, called “flash loans,” to be instantly issued and settled. These loans require no upfront collateral and happen almost instantly.

Aave Protocol governance

Aave, like any other decentralised network, gives its native coin holders the power to vote. However, an AAVE holder must first deposit the native asset in the platform’s safety module account, as explained earlier, to be eligible.

Eligible AAVE holders can thereby discuss, propose, and vote for or against any modification to be implemented on the Aave network.

Liquidators

A liquidation is a process that occurs when a borrower's health factor goes below 1 due to their collateral value not properly covering their loan/debt value. This might happen when the collateral decreases in value or the borrowed debt increases in value against each other. This collateral vs loan value ratio is shown in the health factor.

In a liquidation, up to 50% of a borrower's debt is repaid and that value + liquidation fee is taken from the collateral available, so after a liquidation that amount liquidated from your debt is repaid.

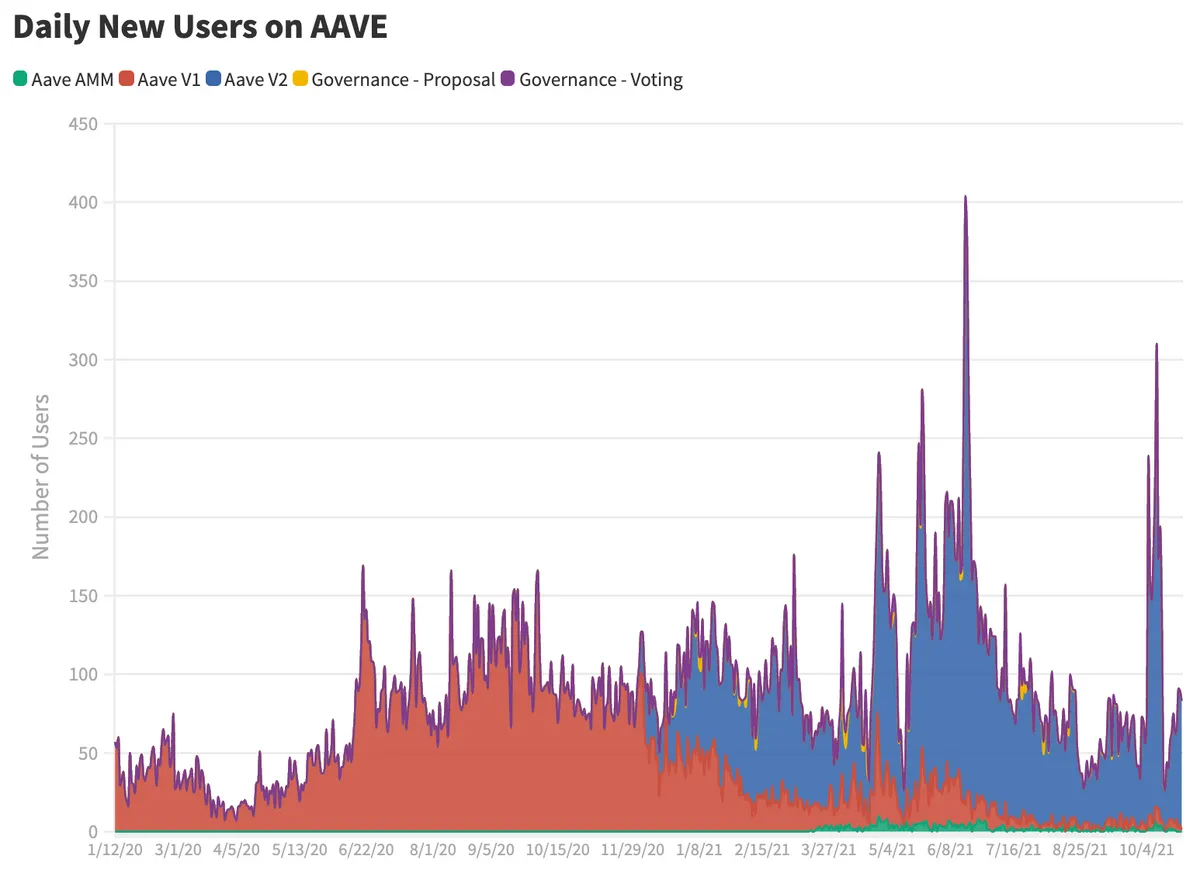

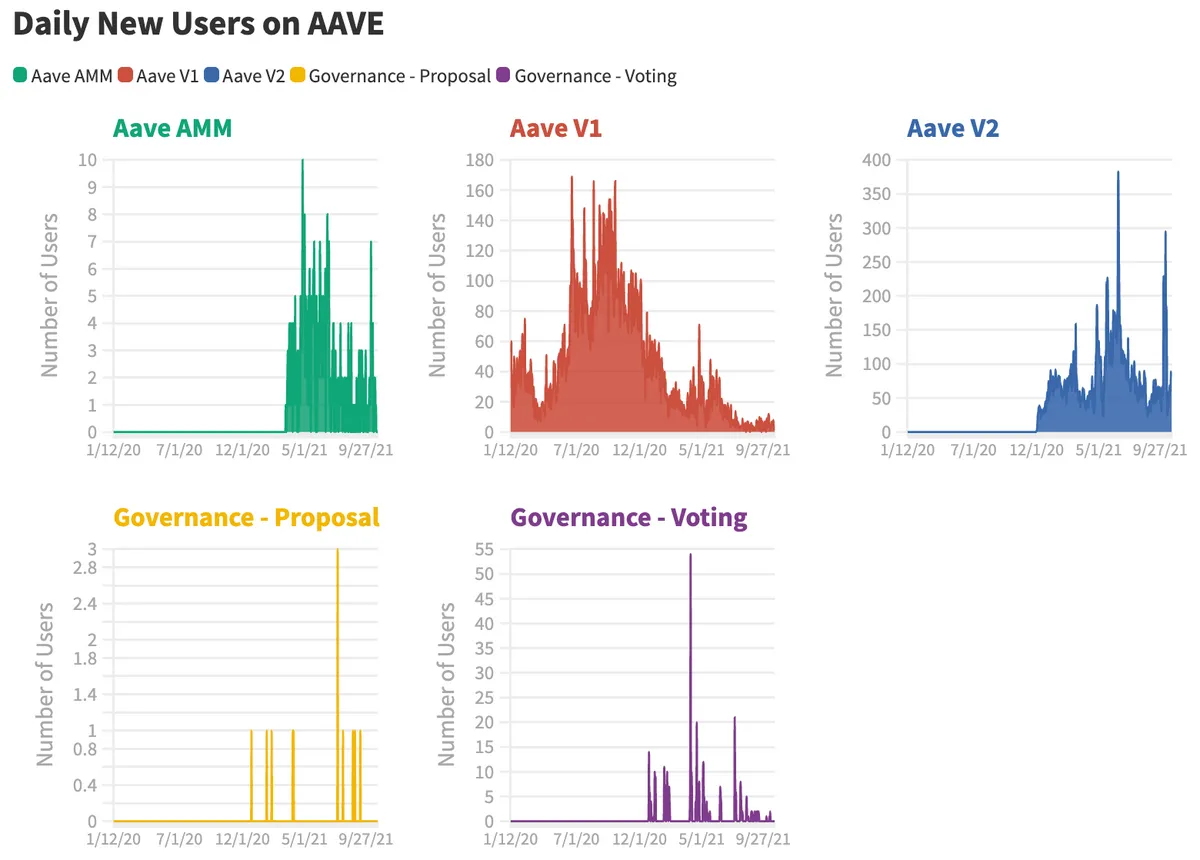

Now, let's look at how each of the AAVE versions have been doing with growth of new users.

> Note: Since The Governance tables don't have an AAVE version specified, I created a new category for them.

AAVE v1 saw a decline of new users while AAVE v2 ramped up

-

After the AAVE v2 launch, the number of users on AAVE v1 saw a sharp decline .

-

AAVE AMM has failed to attract any significant growth and AAVE v1 still attracts more users than AAVE AMM.

- AAVE governance saw a peak of voters in May 2021 with around 55 new voters signing up for AAVE!

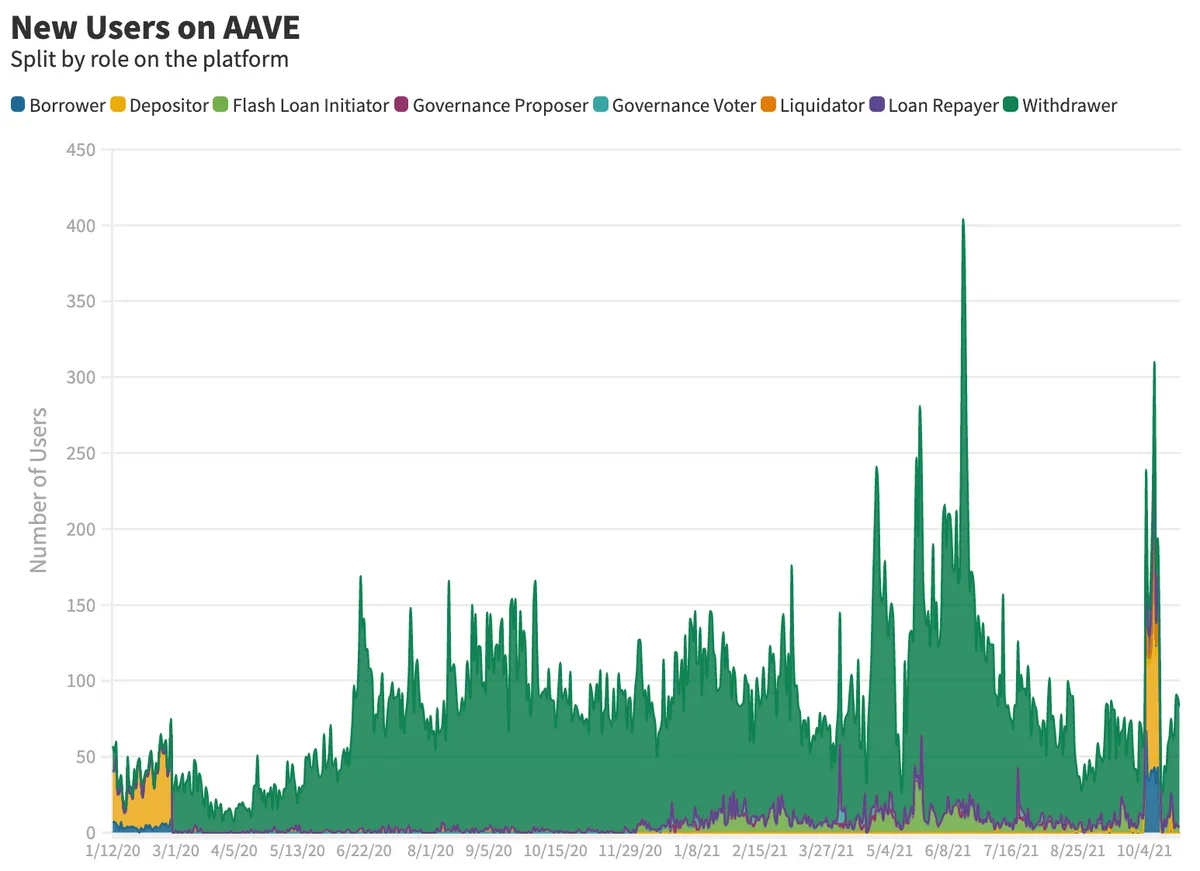

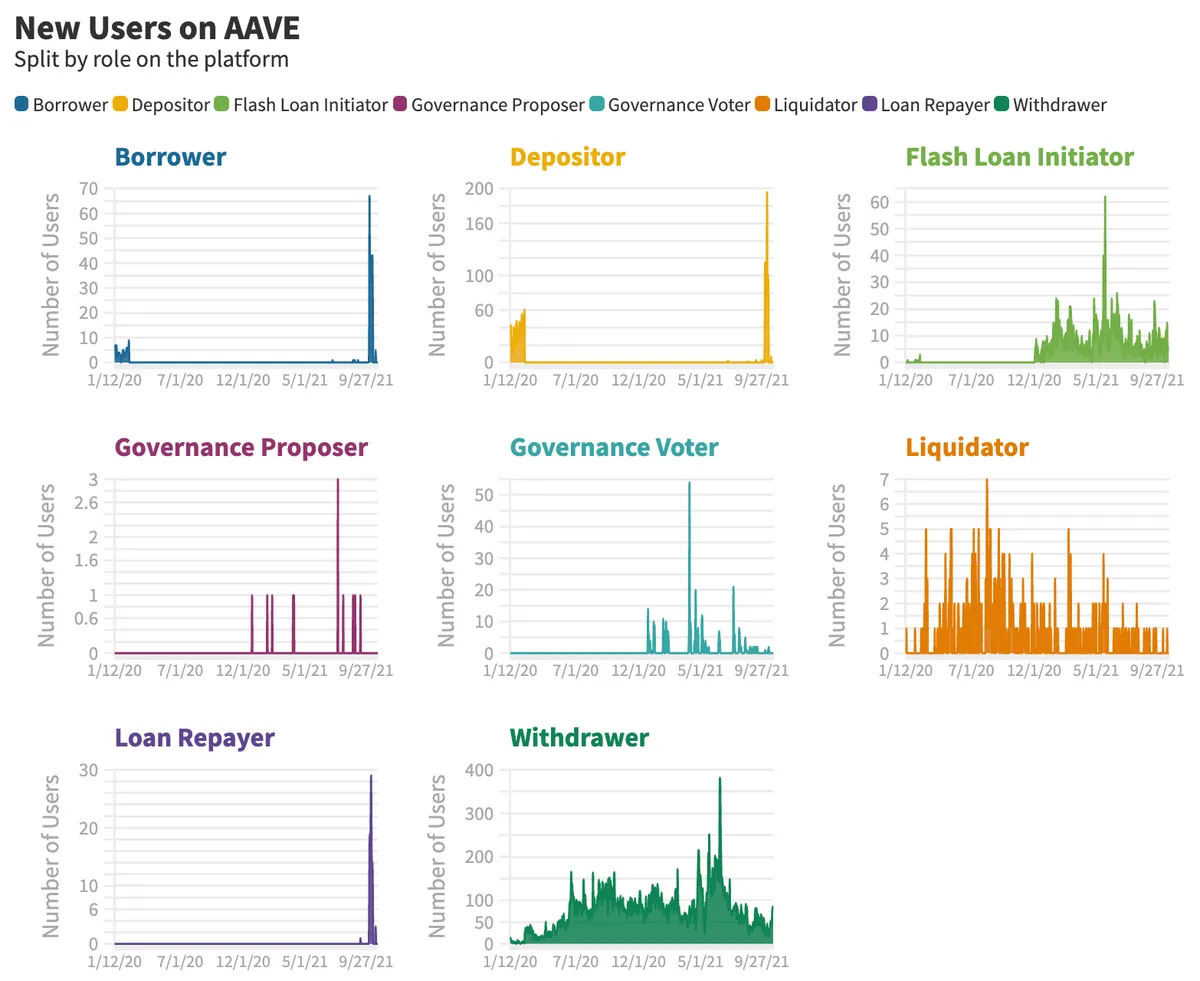

New users split by role on platform

Next, I was planning on splitting users by role on the platform but it seems like there's a good amount of data missing for Borrowers and Depositors looking at the chart between March 1, 2020 and October 4, 2020. The peaks in Borrower and Depositors can only be seen outside of this time period.

Surprisingly, there's been a constant inflow of new Flash Loan initiators on the platform post AAVE-v2 launch :)