Anchor - Financial Imagineering

Anchor Protocol is easily the flagship project and bootstrapping protocol of the Terra Ecosystem. A protocol that incentivises the adoption of UST the algorithmic stable coin. The 20% risk-free APY on UST has been the main driving factor for adoption of Terra ecosystem. Its the lynchpin of Terra ecosystem. Doubtful ?

UST has a marketcap of 10Billion+. However almost 60% of it is deposited in Anchor Protocol.

Like it or not, alot of LUNA's current adoption drive leverages Anchor Yeild. With the onset of Abracadabra's Degenbox strategy, Anchor's Deposit side has been stressed. The borrow side has not been able to sufficiently compensate for the increase in Anchor Earn side's demand. This has been draining Reserves of Anchor. As Anchor team works on going cross chain, the Borrow side of Anchor can't suffer any major losses in terms of Collateral deposited.

In this dashboard, we will look into bLUNA and bETH deposited as collateral, Primarily the distribution of Collateral deposits, analyze it using my good old friend Lorenz Curve

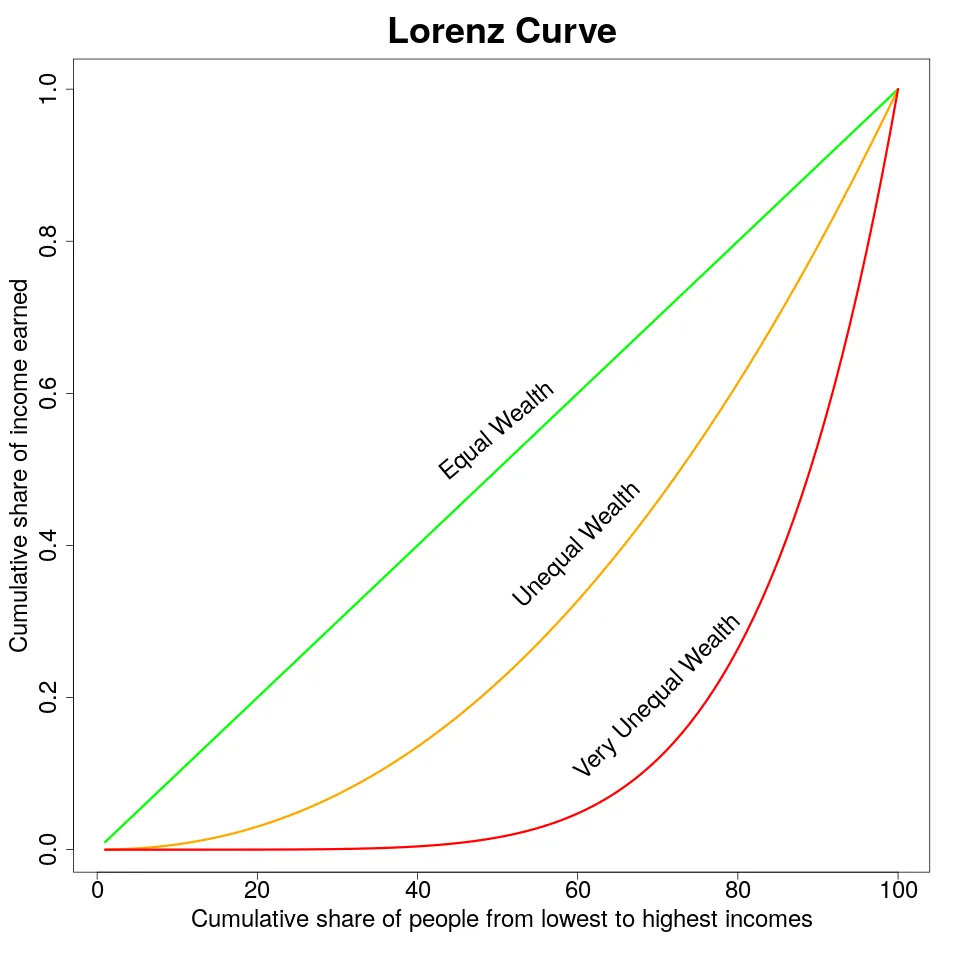

Who is my good old friend Lorenz Curve ?

The Wikipedia copy-pasta implies ->

In economics, the Lorenz curve is a graphical representation of the distribution of income or of wealth. It was developed by Max O. Lorenz in 1905 for representing inequality of the wealth distribution.

The curve is a graph showing the proportion of overall income or wealth assumed by the bottom x% of the people, although this is not rigorously true for a finite population (see below). It is often used to represent income distribution, where it shows for the bottom x% of households, what percentage (y%) of the total income they have. The percentage of households is plotted on the x-axis, the percentage of income on the y-axis. It can also be used to show distribution of assets. In such use, many economists consider it to be a measure of social inequality.

In simple terms, the Lorenz curve shows us the disparity in wealth in the form of the curvature of the distribution. In an ideal world (which doesn't exist) the curvature is zero, i.e its a straight line distribution, which means every person holds similar wealth. The greater the curvature the greater the disparity.

The funny thing about crypto is, there are always intial adopters who tend to accumulate more wealth than normal users. This means, the wealth is almost always skewed. However, this skew could be dangerous for protocols like Anchor, where this wealth skew allows some individuals to wreck the entire protocol. In this dashboard, we will see how bad is this skew and also some top individuals who could wreck the protocol, if they choose to.

Creating Lorenz curve

Creating the Lorenz curve isn't easy, esp on SQL. The idea is to sequence the wealth data, i.e wallets and their associated balances, into wealth buckets (we will use round function to keep the granularity`). These wealth buckets are then arranged in ascending order and cumulative sum is found for each wealth bucket. The cumulative sum will give us the Distribution with respect to each wealth bucket, but that would mean alot of data points, hence we will use percentage of addresses in a wealth bucket, and then rounding it again will give us 100 data points at max.

The data

For this analysis, we will need the collateral balances of every user on Anchor. This can be easily tracked by tracking messages transacted to the Anchor Overseer Contract - terra1tmnqgvg567ypvsvk6rwsga3srp7e3lg6u0elp8. There are only two collateral events we need to track, a Lock Collateral and an Unlock Collateral.

Lock Collateral: Sample transaction hash - 500A71B7441C0F1BC87F1453F637026CE1FDD9F874CDC44B78FC140ED82F83C6Unlock Collateral: Sample transaction hash - 52270774972C6E045B5A7F28FA830F21A88AF71D55E50DF65E5097B0473DF7B7

For Lock collateral:

We can see the lock_collateral call contains the collateral type and amount, with the sender being the user depositing collateral. If the asset is terra1kc87mu460fwkqte29rquh4hc20m54fxwtsx7gp, then the collateral is bLUNA. If its terra1dzhzukyezv0etz22ud940z7adyv7xgcjkahuun then its bETH. Its a similar structure for unlock, however its unlock_collateral being called.

Once these events are collected, a simple user based aggregation will give the current user collateral balances of Anchor.

First we will look into the OG bonded LUNA. How does the Lorenz distribution look like for bLUNA ?

So insights :

- 0.1% of wallets hold 55% of bLUNA deposited as collateral.

- 1 percent of wallets hold 80% of all bLUNA collaterals.

- Top 10 percent of wallets have deposited almost 95% of all bLUNA collateral.

How to read the plot above ?

- x-axis shows the percent of wallets

- y-axis shows the percent of wealth, which in our case is collateral deposited

- So point

(x,y)on the graph will denote the bottomxpercent of wallets holdingypercent of collateral - Subtracting the

xfrom 100 andyfrom 100 will give us the100-xtop percent of wallets holding100-ypercent of collateral.

Who are some of these wallets, and what percent of collateral deposit are theirs ?

The top depositor alone has deposited 22% of all bLUNA collateral. The top 10 wallets alone contribute over 50% of all bLUNA collateralized.

How does the same analysis on bETH fare ?

Insights :

- Atleast ETH is marginally more well distributed that bLUNA.

- The top 0.1% control 43% of all bETH collateralized

- The top 1% control slightly under 70% of all collateralized bETH.

- The top 10% of wallets have 90% of all bETH collateral deposits.

While the Lorenze curve looks better, the top wallets in bETH deposits are much more skewed than bLUNA depositors.

- The top user, controls 30% of all bETH deposited

- The top 5 users control 50% of all bETH deposited as collateral.

What does this mean for Anchor ?

Anchor is a Decentralized trustless Lending protocol. Its 20% risk free APY is its main selling point. It uses the staking rewards from these bonded Collaterals to fund this APY. This means, Anchor Earn depends on a healthy Anchor Borrow. At the current situation, is more like a Benevolent Dictator situation. A group of 10 to 15 wallets controlling 50+% of all collateral deposited, that brings in Earn APY.

The real question is, will these whales put the ecosystem's welfare ahead ? Definitely not. Its the incentives that keep them here. The question arises, what will these Whales do once ANC rewards dry up or the Borrow APR is significantly higher than Earn Deposit APR, a situation which is closer and closer these days. Won't these users move to greener pastures? What will Anchor do to prevent this from happening ? Will more liquid staking opportunities improve the decentralization ?

Losing these players, could be catastropic for Anchor and Terra alike. At the same time, having these large entities, especially two wallets holding 20% collateral supply of each collateral isn't an entirely convincing either.

Creative solutions are needed. The easiest and hopium filled way is to expect more Whales to turn up and reduce the single user concentration at the least. A better way would be to come up with solutions that leverage the vast liquidity locked in Anchor Deposit.

The current CURVE wars need no introduction, are simply governance wars to control CURVE's liquidity flow. CURVE's ability to allow liquidity utilization by CRV rewards, has not only kept up liquidity with limited emissions, but also the resultant high APRs are mostly due to the lack of dilution of CRV's price. Maybe a means to putting the vast Earn reserves to use or coming up with creative means to lock ANC tokens preventing dilution can incentivize more borrowing. While I lack any ideas to come up with, Maybe the bigger brains can help Anchor Protocol as its is at the mercy of such Whales right now.